2025 Social Security Retirement Age:The Social Security retirement age plays a crucial role in determining when individuals can begin receiving full retirement benefits. For those planning to retire in 2025, understanding the nuances of the Social Security system and its rules is essential. This article delves deep into the 2025 Social Security retirement age, explaining eligibility, benefits, and key factors that influence retirement planning.

What is the Full Retirement Age in 2025?

The Full Retirement Age (FRA) for individuals born in 1960 or later is set at 67 years old. This means that if you were born in 1960, you would reach full retirement age in 2027. However, in 2025, individuals turning 62 will become eligible to claim early retirement benefits.

Early Retirement Age

Individuals can opt for early retirement benefits starting at age 62, but this comes with a significant reduction in monthly payouts. The reduction is approximately 30% of the full benefit amount for those claiming at 62 instead of waiting until FRA.

Key Milestones for Retirement Planning

Age 62: Early Eligibility

- In 2025, those born in 1963 will turn 62, making them eligible for early retirement benefits.

- Claiming benefits at 62 results in reduced payments for life but provides immediate financial support for those who need it.

Age 67: Full Retirement Age

- Those born in 1958 will reach their FRA in 2025.

- At this age, retirees are entitled to receive their full, unreduced benefits.

Age 70: Maximum Benefits

- While FRA is 67, delaying retirement until age 70 results in an 8% increase in benefits for each year beyond FRA. This strategy maximizes monthly payouts, providing a higher income stream.

How Benefits Are Calculated

Social Security benefits are determined based on your Primary Insurance Amount (PIA), which is calculated using your 35 highest-earning years. The following factors influence your monthly payments:

- Earnings Record: Higher lifetime earnings result in higher benefits.

- Age of Claiming: Claiming before FRA reduces benefits, while delaying beyond FRA increases payouts.

- Cost-of-Living Adjustments (COLA): Annual adjustments ensure benefits keep pace with inflation.

Impact of Early Retirement on Benefits

Choosing early retirement at age 62 can have long-term implications on your financial well-being. Here’s how benefits are affected:

- Reduced Monthly Payments: For retirees claiming benefits in 2025, the reduction for starting at 62 instead of 67 is approximately 30%.

- Spousal Benefits: If you’re married, spousal benefits are also subject to reductions if claimed early.

- Longevity Risk: Reduced payments may not adequately cover expenses during a long retirement.

Delaying Retirement for Maximum Benefits

Delaying retirement until age 70 offers several advantages:

- Higher Monthly Payments: An 8% increase in benefits for each year beyond FRA can significantly boost income.

- Enhanced Spousal Benefits: Delayed claiming can increase survivor benefits for your spouse.

- Tax Efficiency: By delaying benefits, you may optimize your tax strategy during retirement.

Eligibility for Spousal and Survivor Benefits

Spousal and survivor benefits are essential components of the Social Security system, providing financial support for non-working or lower-earning spouses.

Spousal Benefits

- Spouses are eligible for up to 50% of the higher earner’s benefit at FRA.

- Claiming spousal benefits before FRA results in reduced payouts.

Survivor Benefits

- Widows or widowers can claim benefits starting at age 60 or 50 if disabled.

- Survivor benefits are calculated based on the deceased spouse’s earning record and can be maximized if the higher-earning spouse delayed retirement.

Social Security Earnings Limit for 2025

If you plan to claim Social Security benefits before reaching FRA and continue working, your earnings may be subject to the earnings test:

- Earnings Threshold: In 2025, the limit for earnings before benefits are reduced is projected to be approximately $21,240 (subject to annual adjustments).

- Reduction in Benefits: For every $2 earned above the threshold, $1 is withheld from benefits.

At FRA, this reduction no longer applies, and your benefits are recalculated to account for withheld amounts.

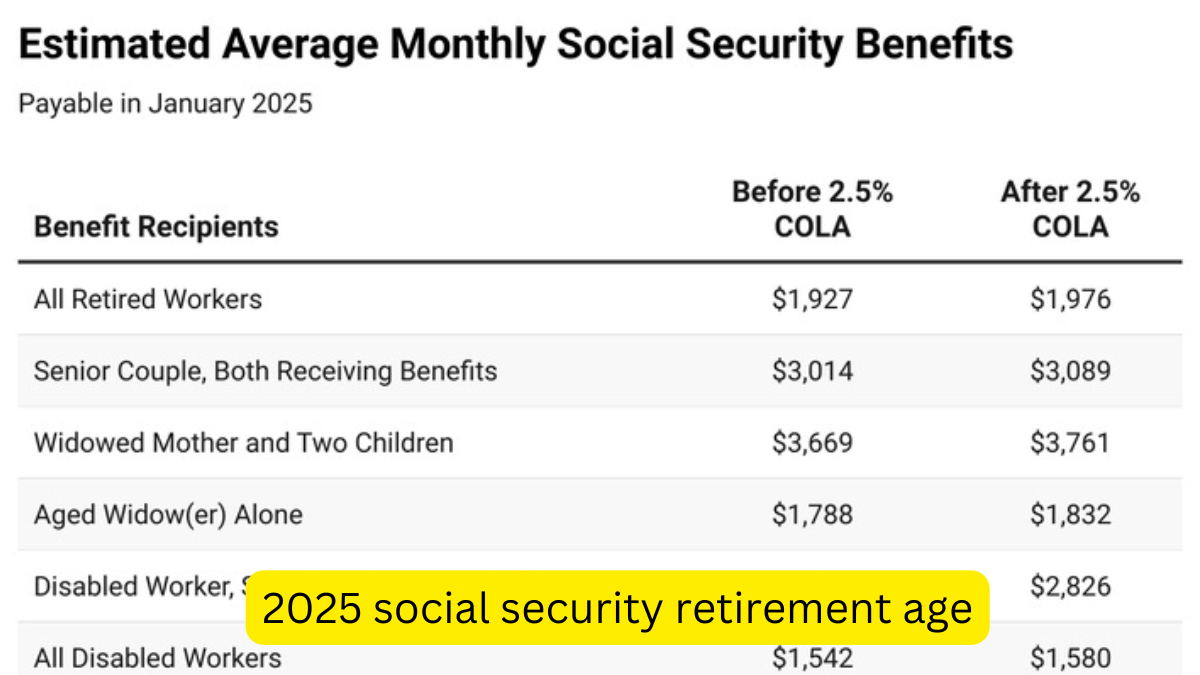

Cost-of-Living Adjustments (COLA) in 2025

COLA ensures that Social Security benefits keep pace with inflation. For 2025, the adjustment is expected to reflect changes in the Consumer Price Index (CPI). While the exact percentage is announced annually, COLA has historically ranged between 2% and 5%, significantly impacting retirees’ purchasing power.

Factors to Consider for Retirement Planning in 2025

- Health and Longevity: If you anticipate a longer lifespan, delaying benefits may be advantageous.

- Financial Needs: Immediate financial requirements may necessitate claiming benefits earlier.

- Employment Status: Continuing to work can affect the timing and amount of benefits you receive.

Strategies to Optimize Social Security Benefits

1. Maximize Earnings Before Retirement

The higher your income during your working years, the higher your benefits will be. Consider working additional years to replace lower-earning years in your 35-year calculation.

2. Delay Benefits When Possible

Waiting until age 70 maximizes your monthly benefits and provides long-term financial stability.

3. Coordinate Benefits with Your Spouse

For married couples, coordinating the timing of benefits can enhance household income and provide greater survivor benefits.

Common Misconceptions About Social Security

- Social Security Will Run Out: While the Social Security Trust Fund faces challenges, benefits are expected to be sustainable for decades, even if adjustments are required.

- Full Retirement Age Means Maximum Benefits: Maximum benefits are achieved by delaying until age 70, not FRA.

- You Cannot Work While Receiving Benefits: You can work while receiving benefits, but early claimants may face benefit reductions due to the earnings test.

Conclusion

Understanding the 2025 Social Security retirement age and its implications is essential for effective retirement planning. Whether you choose to claim benefits at 62, 67, or 70, informed decisions can significantly impact your financial well-being during retirement. By maximizing your benefits and considering your unique circumstances, you can ensure a secure and comfortable future.